The Hidden Stress of Insurance Paperwork: Why Most People Feel Lost

Imagine opening your mail and finding a thick packet from your insurance company. Your heart sinks a little because you know it is filled with complicated words. You try to find out exactly how much you are paying and what is protected.

But the page looks like a foreign language to you. This confusion causes real stress in your daily life. You might worry that you are paying too much for your coverage. Or worse, you might fear that a sudden accident will leave you completely unprotected and broke.

It is a quiet anxiety that many people face every single day. Here are a few reasons why we struggle to find the right answers:

- Many online guides use heavy industry jargon that only makes the confusion worse instead of actually helping you.

- Insurance agents are often too busy to walk you through the fine print line by line, leaving you to guess.

- Misleading articles on social media give generic advice that does not match your specific state laws or policy type.

- People often rely on advice from well-meaning friends who do not understand their own policies either.

- The search for simple, honest answers usually leads to complex sales pitches instead of clear, helpful education.

This constant state of confusion slowly eats away at your financial confidence and peace of mind. Here is how this struggle impacts your mindset:

- You feel vulnerable because you are paying hard-earned money for a service you do not fully comprehend.

- The fear of making a costly mistake can make you avoid looking at your finances altogether, causing more anxiety.

- It makes you feel powerless, as if the big insurance companies hold all the cards while you remain in the dark.

- Without clear knowledge, you lack the confidence to negotiate better rates or switch to a better plan.

- You live with the constant worry that a claim might get denied when you need help the most.

When you do not understand your policy, you are essentially driving in the dark without headlights. Think of your insurance policy as a legal contract. If you do not know the terms, you cannot protect your rights.

Many families find out too late that their policy has giant gaps. For example, a homeowner might think they are covered for water damage, only to learn that flood water is excluded. This realization usually happens during a crisis, which is the worst possible time.

The declaration page is supposed to solve this problem. It is designed to summarize your entire policy on a single sheet of paper. Yet, because of poor formatting and complex terms, it often does the exact opposite.

We want to change that for you today. We believe you should feel confident and secure every time you look at your financial documents. You deserve to know exactly what you are paying for without needing a law degree. Let us break down the walls of confusion together and put the control back in your hands.

Your Clear Step-by-Step Guide to Reading the Dec Page

Locating and Verifying Your Basic Personal Details

Let us start at the very top of the page. This section contains your personal information, and it is more important than you might think. Treat this part like checking your boarding pass before getting on a plane.

You need to make sure your name, home address, and contact details are spelled correctly. Even a tiny typo in your street address can cause massive delays when you need to file a claim. If you spot a mistake, call your agent immediately to fix it.

Check the policy period. This shows the exact date and time your coverage starts and ends. If you are switching policies, make sure there is no gap between the old one and the new one. A single day without coverage can leave you exposed to high financial risks.

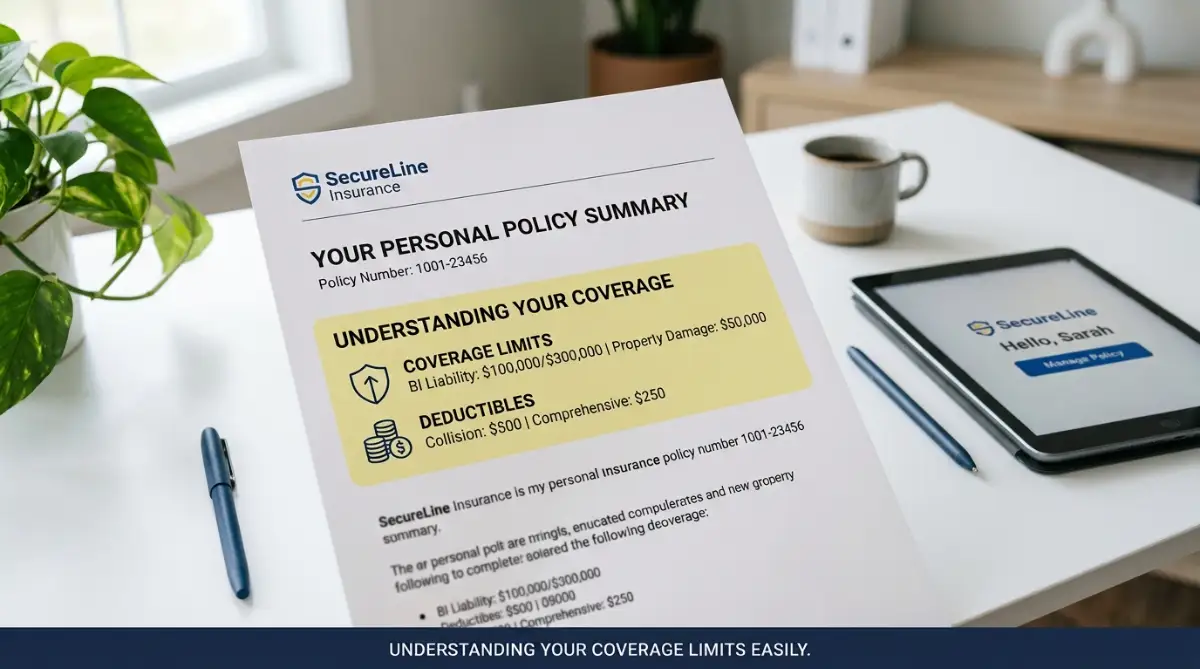

Verify the policy number. This is your unique ID. Keep this number handy because you will need it whenever you call customer service or use your mobile app. It is usually located in bold letters near the top right corner.

Look for listed operators. On an auto policy, this lists everyone who is allowed to drive your car. If a family member is missing from this list, they might not be covered in an accident. Make sure your household drivers are all listed correctly.

Identifying Your Coverage Limits and Policy Exclusions

Now, let us move to the core of the document. This is where you see exactly how much financial protection you have purchased. Think of these numbers as your financial safety net.

Locate the liability limits. These numbers are often written as split limits, like 100/300/100 on an auto policy. This represents the maximum amount the company will pay for injuries and property damage. Let us break down what those numbers actually mean.

The first number is the limit for one injured person in an accident. The second is the total limit for medical bills for the entire accident. The third is the limit for property damage that you caused.

For example, if you cause a three-car crash, the property limit pays to fix the other cars. If the damage costs more than your limit, you must pay the rest out of your own pocket. This is why having high enough limits is so important for your peace of mind.

Check your dwelling coverage. On a home policy, this is the amount of money you get to rebuild your house. Make sure this number matches the actual cost of building a home today, not just the market value of your property. Building costs can rise quickly, and you want your policy to keep up.

Search for exclusions. While the dec page is a summary, it will often point out what is not covered. Look for small notes that mention things like mold, earthquakes, or specific dog breeds. If you see an exclusion you do not like, you can ask for a policy rider.

Deconstructing Your Deductibles and Premium Breakdowns

This is where we talk about the money you pay out of pocket before your insurance starts paying. Understanding this balance is the key to managing your monthly budget.

Find your deductible amount. This is the amount you agree to pay first in a claim. For instance, if you have a one thousand dollar deductible and a car repair costs three thousand dollars, you pay one thousand. The insurance company will then pay the remaining two thousand dollars.

A higher deductible usually means a lower monthly premium. However, you must make sure you have that cash saved in an emergency fund. Do not set your deductible to a level you cannot afford to pay tomorrow.

Look at the premium breakdown. This shows the cost for each specific type of coverage. You might see a separate price for comprehensive coverage and another for collision coverage. This helps you see where your money is actually going.

By looking at these separate costs, you can decide if you want to keep certain optional coverages. For example, if your car is very old, you might decide to drop collision coverage to save money. This visual breakdown gives you the power to customize your policy.

Check for discounts. Many companies list the discounts applied to your policy right here on the page. Look for things like safe driver discounts, paperless billing, or multi-policy bundles. If you do not see a discount you deserve, call your insurer and ask about it.

How to Spot Hidden Fees and Endorsements on Your Page

Sometimes, insurance policies have extra additions called endorsements or riders. These are changes to the original policy that either add or remove coverage. They are highly important to spot because they modify your main contract.

Look for the policy change section. This is usually located near the bottom of your declaration page. It might list specific codes that refer to longer documents in your main packet. Do not ignore these codes because they change your coverage.

For example, you might see a code for a jewelry rider. This means your high-value items are covered beyond the standard limits of a regular policy. It ensures your most precious belongings are safe from loss.

Check for administrative fees. Some companies charge small fees for payment plans or paper statements. Knowing these fees helps you avoid paying extra money every month. You can often remove these fees by signing up for automatic payments.

A Real-Life Example: Sarah’s Car Insurance Confusion

Let us look at a simple story to see how this works in real life. Sarah received her new car insurance packet and almost threw it in a drawer without looking. She used to find insurance documents incredibly boring and hard to read.

However, she decided to spend five minutes reading her declaration page instead. She noticed that her deductible was set to one thousand dollars, which was higher than she remembered. She knew her savings account could not handle that right now.

Sarah realized she did not have that much money in her emergency fund. She called her agent and lowered her deductible to five hundred dollars, adjusting her budget accordingly. The small increase in her monthly payment was worth the safety.

Two months later, another driver backed into her car in a parking lot. Because she checked her dec page, she knew exactly what to expect and faced zero financial surprises. Taking those five minutes saved her from a major financial headache.

Why It Pays to Keep a Physical Copy of Your Summary

In our digital world, it is easy to rely completely on mobile apps to view your insurance information. However, having a printed copy of your declaration page is highly recommended. You never know when technology might fail you.

If you get into an accident in an area with poor cell phone service, you might not be able to log in. Having a physical paper in your glove box or home safe ensures you always have access. It is a simple backup plan that costs nothing.

It also makes it easier for family members to find your policy details in case of an emergency. A quick glance at a piece of paper is always faster than searching through a locked phone. Keep your papers organized, and you will always feel prepared.

Let us take your insurance knowledge to a higher level. When you receive your package, knowing how to spot specific policy details can save you thousands of dollars. You can learn more about understanding your policy declaration page to see how insurance companies organize your basic data.

Many state governments provide consumer safety guides to help protect your financial rights. You can search the National Association of Insurance Commissioners database to find specific rules for your local area. This is a great way to verify if your current policy meets local legal standards.

If you are planning to buy a home soon, your insurance policy details are highly important. For example, lenders will carefully examine your coverage limits when managing your debt-to-income ratio during a mortgage application. Ensuring your declaration sheet shows clean, accurate coverage will keep your home-buying process on track.

Now, let us discuss how to look past the surface of your paperwork. If you do not look at the fine details, you might miss errors that cost you cash. We want to make sure you have the exact tools to review your policy like an expert.

Pro-Level Secrets to Master Your Policy and Save Money

Comparing Your Coverages and Tracking Hidden Add-ons

One of the best secrets of insurance experts is to do a line-by-line comparison every time your policy renews. Do not just look at the total premium cost at the bottom of your sheet. Instead, check the price of each individual line item to see if the cost went up.

If you notice that your comprehensive car insurance premium has jumped significantly, ask your agent why. Sometimes, companies add tiny fees or emergency roadside coverages that you do not actually need. By catching these small changes early, you can keep your monthly bills under control.

Leveraging State Insurance Rules and Free Consumer Tools

Every state has an insurance commissioner office that protects consumers from unfair pricing. You can use their free online calculators to see the average rates in your specific neighborhood. If your declaration sheet shows a much higher price, you have the leverage to negotiate.

We always suggest asking your agent to run a new market search using your clean driving or claims history. Often, they will find discounts that were not automatically applied to your account. This simple check can put money back into your wallet with just one quick phone call.

Maintaining Your Protection Habits for the Long Run

To keep your protection strong over the years, you need a simple review routine. We recommend scheduling a ten-minute insurance audit twice a year. Mark this on your calendar during major seasonal changes so you do not forget.

During this quick check, compare your current assets to the limits shown on your paper. If you bought new expensive items or paid off a loan, your coverage needs to change. Keeping your paperwork updated ensures you are never underinsured during an emergency.

Tracking Asset Changes and Liability Adjustments

As your personal net worth grows, your standard coverage limits might not be enough. If you get sued after a major accident, a court can go after your personal savings. This is why matching your policy limits to your actual wealth is a smart financial move.

You should always make sure your liability coverage is equal to or greater than your total assets. If your limits are too low, you are leaving your future savings exposed to risk. Adjusting these numbers on your dec sheet is a quick fix that offers massive peace of mind.

Dangerous Pitfalls: Five Mistakes Most People Make with Their Dec Page

Setting Deductibles Too High Just to Save Money

It is true that raising your deductible will lower your monthly payments. However, setting this number too high is a dangerous gamble that many families lose. If you cannot afford to pay your deductible during a sudden emergency, your insurance is practically useless.

For example, if your home roof is damaged and your deductible is five thousand dollars, you must pay that amount first. If you do not have that cash ready, the repair work cannot even begin. Always choose a deductible that matches your actual emergency savings.

Failing to Update Your Policy After Remodeling or Home Inspections

Many people remodel their kitchens or add new rooms without telling their insurance company. This is a massive mistake because your home coverage limit is based on the old house structure. If a fire occurs, your policy will not pay to rebuild the new, expensive parts of your home.

To avoid this, you should look for identifying home inspection warning signs before starting any major home improvement project. Keeping your insurer updated about these changes guarantees that your entire house is protected. It also prevents claims from getting delayed or rejected later on.

Relying on the Same Policy Year After Year Without Checking Rates

Many people believe that staying with the same insurance company for decades guarantees the best price. This is a common myth that can cost you hundreds of dollars every year. Insurance companies often raise rates slowly over time, a practice known as price optimization.

If you do not shop around, you might be paying much more than a new customer for the same coverage. We recommend checking competitor rates at least once a year to keep your current company honest. This simple step ensures you are always getting a fair deal.

Not Verifying Your Named Insureds and Listed Drivers

Another common error is having incorrect names listed as the primary owners on your sheet. If you get married or buy a car with a partner, both names must be listed correctly. If a claim is filed under a name that does not match the car title, the company can deny the claim.

This rule also applies to teens or roommates who drive your vehicles. Make sure every regular driver in your home is explicitly listed on your paper. Taking a few minutes to check these names will save you from major legal stress.

Assuming Your Policy Automatically Covers Natural Disasters

Many policyholders assume that standard home insurance covers every type of natural disaster. This is a dangerous mistake that leads to massive financial losses every year. Standard policies almost always exclude damage from floods and earthquakes.

To get this protection, you must buy separate policies or add specific endorsements. Always look at your declaration sheet to verify if natural disaster coverage is active. Knowing your limits before the storm hits is the best way to protect your family.

Your Next Steps Toward Absolute Insurance Confidence

Now you have the knowledge to take control of your financial protection. Reading your policy declaration page does not have to be a stressful or confusing chore. By spending just ten minutes reviewing these details, you can protect your hard-earned money and secure your family.

Think of your insurance document as a map for your financial security. When you understand the map, you can avoid costly wrong turns and build a safer future. This habit is just as important as protecting digital assets with security steps to keep your money safe online.

If you run a small business, managing your insurance paperwork is also similar to managing business cash flow issues to prevent sudden failures. Both require you to look closely at the numbers and plan ahead. Taking action today is the absolute best way to secure your hard-earned progress.

We encourage you to go find your current declaration page right now. Open it up, find your deductible, and verify your coverage limits today. You will feel a sudden wave of confidence knowing that you are in complete control of your financial future.

Expert Insurance Advice:

01. Compare More Than the Premium:

A low premium may look attractive, but it doesn't always provide the best value. Review coverage limits, deductibles, exclusions, and customer support before making a decision.

02. Read Real Customer Experiences :

Customer reviews can reveal how an insurance company handles claims and support. Look for consistent feedback across multiple trusted sources instead of relying on a single rating.

03. Understand What's Not Covered:

Every insurance policy has exclusions. Reading the fine print helps you avoid unexpected surprises when it's time to file a claim.

04. Check the Claims Process:

A reliable insurance provider should offer a simple and transparent claims process. Fast claim handling and clear communication are often signs of quality service.

05. Review Your Policy Regularly:

Your insurance needs can change over time. Reviewing your policy each year helps ensure your coverage still matches your current lifestyle, assets, and financial goals.

A Quick Laugh

The Dangerous Hobby

An insurance agent was helping a man fill out a life insurance application.

The agent asked, "Do you participate in any highly dangerous activities or hobbies? For example, skydiving, rock climbing, or scuba diving?"

The man shook his head and replied, "No, not really. But sometimes I eat leftovers from the fridge without smelling them first."

Disclaimer:

The information provided in this article is for educational and informational purposes only. It should not be treated as professional financial, legal, or insurance advice. Insurance policies, terms, and coverage options vary greatly by provider and location. Always consult with a licensed insurance agent or qualified professional before making any decisions regarding your insurance coverage.